An Introduction to the Innovations: Juhudi Kilimo and Kiva

Where foreign aid fails to promote financial inclusion – opting instead for high-level allocation systems – microfinance institutions have a unique capacity to reach into the populations in developing countries in a way that fosters economic inclusion and builds financial capacity and responsibility. Despite both being involved in ‘microfinance operations,’ Juhudi Kilimo and Kiva present very different organizational models, development models, forms of scaling, and impact. These differences aside, each organization displays a strong commitment to fostering positive impact amongst the populations they serve.

Juhudi Kilimo – investing in farmers

A Kenyan mother was able to invest in dairy cows that provide food security and a sustainable income for her and her family (source: Juhudi Kilimo ppt).

Juhudi Kilimo is a Kenyan based microfinance organization founded in 2004, and began lending in 2006. It is projected to reach 100,000 rural farmers by 2015. It approaches the microfinance market with a very new model that funds productive agricultural assets. It targets a rural population of 9.6 million individuals in Kenya that earn between 1 and 4 dollars per day, and own 1-5 acres of land. Almost the entirety of this population subsides on agriculture, and is composed predominantly of women. Considering that 23 percent of the adult Kenyan population is serviced with micro finance,[ref]Juhudi Kilimo. MFTransparancy Seal of Transparency Award (2013). Retrieved February 7th, 2014, from http://juhudikilimo.com/juhudi.php?id=33.[/ref] one can reasonably beg the question: what is significant about another microfinance institution? Adaptation. This is simple word, but it carries with it large benefits. It is through adaptation of financial models and continuous regard for its clients’ needs that Juhudi Kilimo has become a successful and responsible microfinance institution.

Juhudi Kilimo is an innovative financial technology that disrupts the preexisting industry on two levels. First, it disrupts the traditional money-lenders who offer loans at extremely high interest rates. At the same time, it disrupts the preexisting microfinance institutions both in terms of the model used and to some extent, the interest rates it offers. There are four key aspects to the innovative nature of Juhudi Kilimo’s financial model:

- Funds productive agricultural assets

- Client isn’t liable to service loan until asset becomes productive

- Loan allows client to purchase higher quality asset than is attainable without loan funds.

- Loans are collateralized – asset acts as collateral against loan.

By only funding agricultural assets – and further, assets that are determined to meet the specific needs of a given client – Juhudi Kilimo is effectively able to skirt a key issue of standard microfinance practices: funding productive agricultural assets guarantees the loan is spent on the agreed upon asset. It also ensures that the borrower has a steady income from the asset to service the loan. The assets that Juhudi Kilimo funds range from dairy cows, other livestock, irrigation systems and farm infrastructure, to farm and farm-to-market transportation. It places an especially strong emphasis on the funding of dairy cows, which serves a family in many ways. First, it provides an additional form of sustainable food security and nutrition. It also provides economic opportunities by selling the excess milk. This example helps illustrates points two and three. The client isn’t responsible for servicing the loan until the asset becomes productive. For example, the client needn’t begin payments on a loan for a diary cow until the cow begins to produce milk. Further, the loan scheme allows the client to purchase a higher quality and producing asset than would otherwise be possible. For example, a client that would otherwise be able to purchase a local Zebu cow (cost: $230) that produces 3 liters of milk a day or an income generation of $1 per day, is enabled by the loan to purchase a Hybrid Friesian cow (cost: $500) that produces 12 liters of milk a day or $4 of income potential per day. In one year, the higher producing cow is able to generate $763 in profits. To date, this has amounted to 54 million liters of milk worth $12.6 million in farmer income.[ref]Juhudi Kilimo. GSBI Accelerator Program Presentation. PowerPoint.[/ref]

Without a Juhudi Kilimo loan, families opt for the domestic Zebu cow, which has 1/3 the economic impact of the hybrid Friesian cow (source: Juhudi Kilimo ppt).

Juhudi Kilimo loans enable farmers to purchase this hybrid Friesian cow, which provides both food security and an alternative source of income for the family (source: Juhudi Kilimo ppt).

Perhaps the most notable feature of Juhudi Kilimo’s model in comparison to other microfinance operations is its innovative use of the funded asset as collateral against the loan, thereby making it safer for the lender. While this acts as a form of protection against default for Juhudi Kilimo as a lender, it also imbues a sense of responsibility amongst the borrowers, who benefit greatly from the dairy cow, irrigation system, or other forms the asset might take. This use of the asset as collateral both protects the lender and incentivizes the borrower to service the loan with the funds derived from the asset

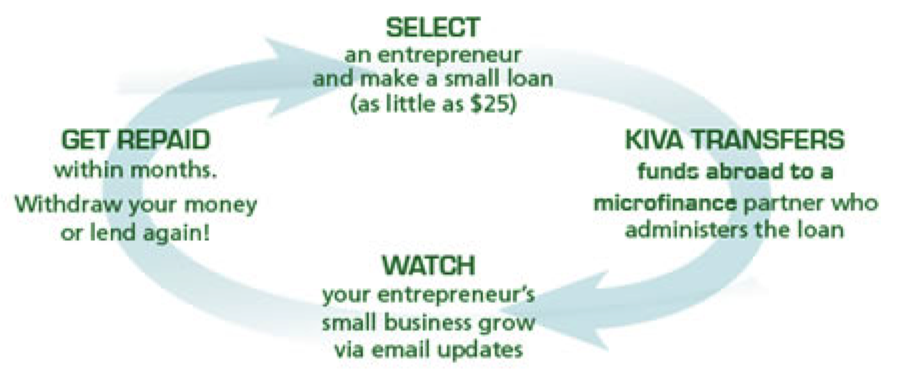

Kiva – loans that change lives

Founded in 2004, Kiva’s lending platform has facilitated 1,252,704 transactions to individuals in the developing world, amounting to US$536,105,250.[ref]Kiva. Statistics. Retrieved Feb 18th, 2014, from http://www.kiva.org/about/stats.[/ref] Also driven by the motivation to improve the lives of those in developing countries, Kiva partakes in microfinance lending, but its means of doing so are very different from Juhudi Kilimo’s asset backed financing. Compared to Juhudi Kilimo’s practice of funding productive assets in a financial agreement between the organization and an individual, Kiva is pioneering an innovative form of person-to person lending focused on business creation.

Kiva successfully leverages an internet platform to connect individual lenders – people like yourself – to people in need of financing, anywhere in the world.

First and foremost, Kiva is non-profit online lending platform that enables individuals to lend money to people in the developing world. In this, Kiva is not a traditional microfinance organization with its own loan portfolios. It works on the basis of microfinance organizations in developing countries posting profiles of their loan applicants onto Kiva’s website. Individual lenders can then browse by geographical region, project, and associated MFI, as well as view it’s rating. In addition to leveraging an Internet platform, transactions from lenders to borrowers are facilitated through PayPal. This innovative online lending enables three key aspects that are integral to Kiva’s success to date:

As a single mother of 6, a $1,950 loan to Kulumkan helps her buy calves for her animal husbandry business, the sole source of income for her and her family. Read more about Kulumkan or how to donate to her or other Kiva users here.

Few geographical constraints. As an online lending platform, Kiva targets a population that is much larger that an in-country MFI is able to target. Yet the Internet rarely acts as a constraint – rather than lending directly to the individual, Kiva works with local partner MFIs that distribute funds to the individual borrowers (see Juhudi Kilimo as example).

Risk tolerant funding source. Individuals or commercial institutions that typically invest in microfinance operations do so largely for a return on investment. By leveraging individual internet users as lenders of small amounts, Kiva is accessing a population that is comparatively risk-tolerant. This population has great potential, and continues to grow.

Transparency of success and failures. By engaging in an online lending platform, Kiva enables high levels of transparency about its partner MFIs; not just about their successes, but also their failures. This is done through an online rating system that is visible to all individuals interested in lending through the given MFI. The potential in this doesn’t stop here. The majority of MFIs in the world, termed “long-tail MFIs” – amounting to nearly 10,000 –are relatively small and non-transparent. For this reason, many investors avoid these institutions. Kiva, on the other hand, is able to partner with these institutions in a transparent way by using the Internet as a ‘reputation-building mechanism.’[ref]Flannery, Matt. “Kiva and the birth of person-to-person microfinance.” Innovations 2.1-2 (2007): 31-56.[/ref]

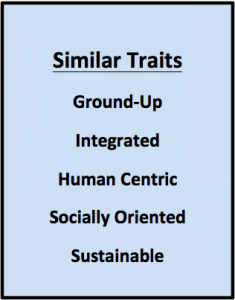

Different Models, Similar Traits

Despite drastically different models, both Juhudi Kilimo and Kiva are able to successfully and sustainably serve those in need. In doing so, each has advantages and disadvantages. For example, by crowd-sourcing capitol, Kiva is able to have a much larger financial impact and borrower population than Juhudi Kilimio with a less resource-intensive model. However, in doing so it risks not monitoring specific loans and their impact, as Juhudi Kilimo is able to do with its very personalized lending scheme. This personalized lending scheme enables Juhudi Kilimo to target a specific population (rural farmers), whereas those funded through Kiva’s platform are at the discretion of the individual lenders.

A unique innovation that both organizations successfully employ is the [relative] elimination of risk from their models. Juhudi Kilimo eliminates excessive risk by collateralizing its loans with the agricultural asset its funds are used for, whereas Kiva uses funds from private individuals, who assume the risk. Kiva’s ability to mitigate risk is only possible because of the small amounts that individuals commit, compared to the large amount that Juhudi Kilimo’s financial partners commit.

With two very different models, both organizations have achieved considerable successes in their relatively short lifespan to date. Within five years from its first loan, Juhudi Kilimo had reached 22,000 rural Kenyan farmers with loans tailored to their specific needs.

The success of both Juhudi Kilimo and Kiva is due in part to their innovative financial technologies, but also a result of many similar traits that guide both social ventures. The traits they both share enable them to successfully carry out their missions, and address the many inadequacies of bilateral and multilateral aid.

Most notably, both foster ground-up development. Loans administered through Kiva might fund a small-scale Nicaraguan business woman, a Kenyan farming collective, or a buffalo herder in Pakistan. Juhudi Kilimo focuses almost solely of rural livelihood development. Its projects might include agricultural irrigation in Nkubu, or the purchase of Chickens for egg production.

Also, both organizations are integrated and human centric, though in different ways. The basis for these traits is that both organizations prioritize the needs of the borrower; Kiva is a platform for loans that fund business projects specific to the individuals’ needs. Juhudi Kilimo, by contrast, works very closely with the Kenyan farmers to determine what agricultural assets will yield the greatest positive impact in their lives. In this, Kiva displays integration in the way of connecting all actors – individual lenders, domestic MFIs, and borrowers – from all reaches of the globe into a meaningful transaction that fosters financial inclusions. Juhudi Kilimo is integrated in a very different way: it integrates its organization by means of loan officers, community groups, and even its new education programs for borrowers (as will be discussed further).

Most fundamentally, both organizations are socially oriented and offer sustainable development rather than profit driven models. Again, they each present these traits while employing very different practices; Kiva is technically a non-profit organization, while Juhudi Kilimo is for profit. Despite the different social entrepreneurship models, both present a strong commitment to creating social impact rather than profit seeking. Kiva commits itself as a ‘non-profit organization with a mission to connect people through lending to alleviate poverty.’ Similarly, Juhudi Kilimo strives to ‘provide market driven, wealth-creating financial services that empower smallholder farmers and rural enterprises to create sustainable agri-businesses and improve their livelihoods.’

These similar traits considered, we will now turn our attention the different ways in which each organization serves its target populations, with an emphasis on their respective scaling models.