Chain Inc. Company Overview: Chain Inc. partners with leading financial institutions to build and deploy blockchain networks that enable seamless, programmatic and peer-to-peer transfer of digital assets. The platform, which is based on the open and interoperable bitcoin protocol, enables institutions to create, issue, store and transfer digital assets on private networks purpose-built for a given market. Founded in 2014, Chain Inc. is headquartered in San Francisco, CA. Chain Inc. Venture Funding: The company has raised $43 million in equity funding from a syndicate of financial and payments industry leaders including Visa, Nasdaq, Citi Ventures, CapitalOne, Fiserv and Orange.

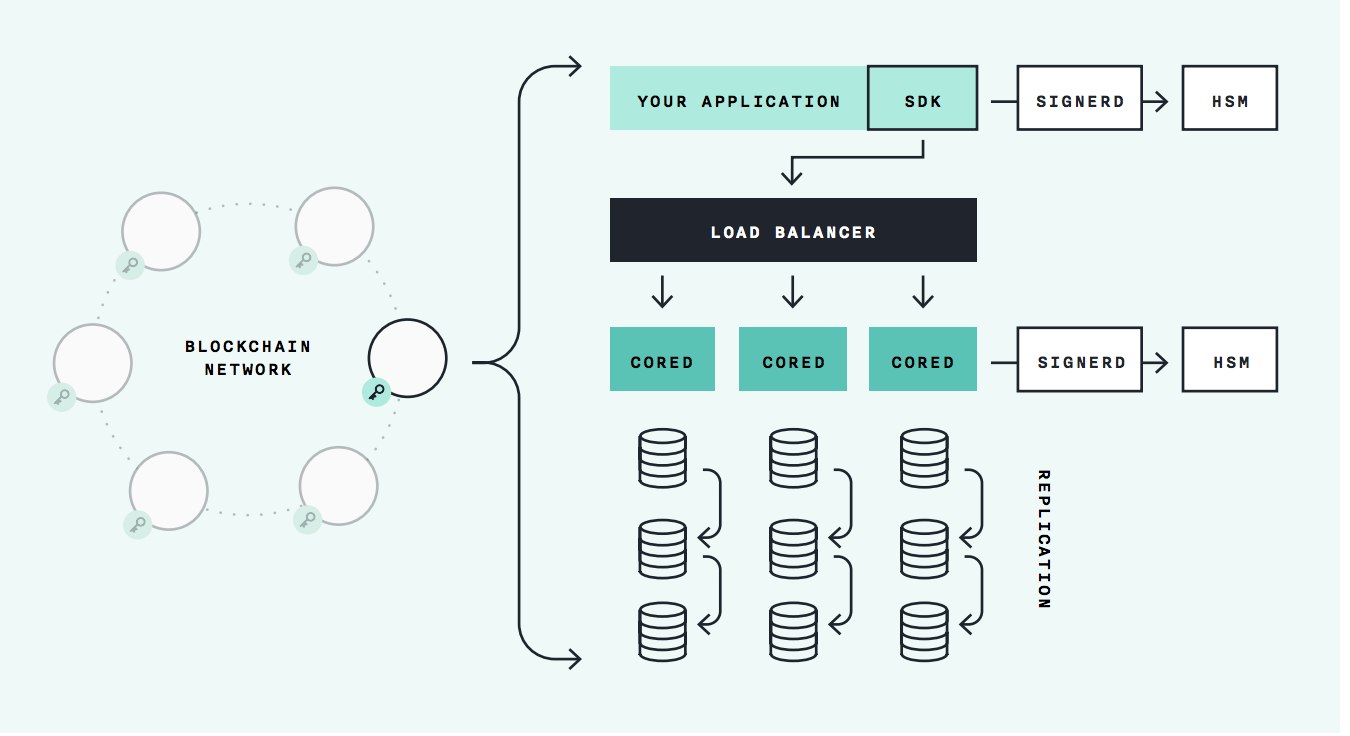

Chain Inc. Product (Chain Core): Chain Core is an infrastructure software that enables institutions to issue and transfer financial assets on permissioned blockchain networks. Chain Core is engineered for the performance demanded by modern financial systems. The time to create, finalize, and settle a transaction is measured in milliseconds. Because its goal is to modernize the backbone of financial services, Chain Core supports today’s volume of transactions and beyond. Scalability is a key design principle of Chain Core. The image below is displays the architecture of Chain Core.

Chain Core Features:

- Chain Core enables organizations to launch and connect to blockchain networks that operate on the open source Chain Protocol.

- Chain Core-enabled blockchain networks facilitate transactions between entities directly. These transactions can serve to issue new assets, transfer assets between parties, or retire assets.

- Chain Core also allows entities to originate assets and issue them onto a network.

- Chain Core uses cryptographic public/private key pairs to keep track of identities, accounts, and ownership.

References:

- https://www.crunchbase.com/organization/chain-2#/entity

- https://chain.com/technology/