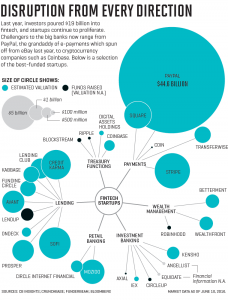

Citigroup has recently been focused on figuring out how to counter the challenges that the fintech companies are bringing, as these new startups are penetrating almost all of the functions that traditional financial banks offer. This is an important step to combat their threatened business, and Citigroup is taking a smart approach when dealing with the tech startups. CEO of Citigroup, Stephen Bird, decided to create an elite group within Citi of about 40 employees from varying backgrounds. Their purpose is to work on projects in a rapid manner. In 4th quarter of 2016, they were able to release a new version of their mobile banking app, after only 10 months of development. Historically, this project would have taken years to complete. Because financial institutions offer so many services, it may be hard to understand how fintech startups can disrupt almost all the aspects of their business. This graphic shows which areas are being affected by fintech companies.

One way that Citi is evolving to keep up with fintech competitors is by having their new mobile app have open architecture, allowing customers to have access to the best functions of the fintech apps. Interestingly, Citigroup may be most vulnerable to fintech companies, as 51% of their revenue come from consumer banking. Their analysts view this area as the most vulnerable. This may be a reason that is spurring Citigroup to adapt to their new challenges.

Article Link: http://fortune.com/citigroup-fintech/