Like the traditional financial banking industry, the insurance industry has not seemed to have changed much over the years. However, InsurTech is trying to revamp the industry from innovations in tech that will allow them to provide value added processes for customers. Efficiency is one area that can be improved to help engage the customer. Anywhere from claims to policy management, a seamless experience can be provided for the customer. Insurers have historically dealt with a lot of data that has to be recorded and analyzed to draw conclusions from. Automation and artificial intelligence will allow insurance carriers to have the tools to make better and quicker decisions. In terms of a distributed ledger technology, insurers are looking into this area which may allow for automation in claims. Ultimately, technology that has helped make other industries more efficient with machine learning, language processing, and better data management is allowing insurance to improve. In addition, InsurTech companies will be able to segment the market to offer niche products. Interestingly, Slice launched an insurance product for users of AirBnbB, the homesharing service. Whether a new insurance companies dominate the market in the future, or current insurance companies implement new technology into their business, I believe this will be very useful and efficient for customers.

Fintech Investment Soars in 2016 around the Globe

Global FinTech investment soared in 2016 to 17.4 billion dollars, an 11% increase from the previous year. The interesting comparison came between the leaders, U.S. and China, with 6.2 billion dollars for 650 deals and 7.7 billion dollars for 28 deals respectively. I believe this distinction is something worth exploring about the two countries. The most reasonable explanation is that U.S. investors are more willing to invest at early stages in the FinTech startups for less money initially. This strategy offers greater risks and greater rewards for the daring investors that choose to take this route.

Ant Financial led all firms with a massive 4.3 billion dollar venture round, the largest in history. This high valuation can most likely be attributed to the many acquisitions and the announcement of the company’s large debt fund. It was also interesting to see the heavy impact that Brexit had on markets, resulting in a 34% decline in FinTech investment.

All in all, this article had promising results when reflecting on the 2016 FinTech investments further illustrating its trending value. When selecting an article, I was wavering between this article regarding the noteworthy investments increase and another article that discouraged anyone thinking of starting a FinTech startup. The drastic differences in the two articles showed the varying opinions surrounding FinTech and, furthermore, the risk/reward associated.

http://www.forbes.com/sites/lawrencewintermeyer/2017/02/17/global-fintech-vc-investment-soars-in-2016/#27b2c5ad434a

Jumping Into the Fintech Industry Too Quickly

Most can see the bright potential and future ahead for fintech. However, this article points out how many up-and-coming fintech companies will fail because of the incessant need in today’s industry to say “yes” to customers. Pleasing the customer and giving the best customer experience is at the top of the priority list for many companies. And however good this strategy might be in practice, John Maxfield warns companies of the risk this strategy leaves companies vulnerable to. Specifically, in banking and loans/lending. Studying the history of banking should be a very common practice, especially considering what the economy went through in the past 10 years. However, companies are priding themselves more now than ever (specifically lending firms) on getting customers tens to hundreds of thousands of dollars in loans within just a week or two. Maxfield warns that the lack on in-person experience with the customers is an alarming move for the industry. The amount of money that is being loaned and transferred without the company ever really knowing where it is going is setting companies up for fraudulent behavior. I think Maxfield has a great viewpoint on this topic. Although companies should continue to be innovative and work to improve customer experience, we all need to be cautious of what the realities are for our society.

https://www.fool.com/investing/2017/02/08/lessons-for-fintech-from-the-history-of-banking.aspx

PayPal launches Slack bot for peer-to-peer payments

About a week ago, PayPal launched its first bot for users of team messaging app, Slack. The bot lets people send peer-to-peer payments for up to $10,000 in a single transaction.

The bot is available as a Slack app through the company’s online directory. It can be used by typing “/PayPal” followed by a command once it’s installed. For example: “/PayPal send $5 to @Michelle.”

As people are turning away from cash and moving towards making payments digitally, PayPal is trying to capitalize on this growing demand for P2P payments. Because Slack already engages 5 million daily active users, PayPal has made a strategic move to launch a bot on its platform and take advantage of their growing user base and the company’s potential growth and expansion. With this, PayPal is ahead of the game and is hoping to establish itself as the payment service of choice for Slack users. I think there is great potential for this bot. Since Slack is usually used at work, I can see this being popular among co-workers. Co-workers can use the bot to split a lunch order for a team outing, coffee morning runs, or splitting a cab fare, and other quick P2P payments. I think this bot is promising since it will allow Slack users to send money without ever having to leave the messing app. This provides Slack users with more of an incentive to use the bot versus other P2P platforms like Venmo.

Source: http://www.businessinsider.com/paypal-adds-p2p-bot-for-slack-2017-2

Are Fintech deal sizes shrinking?

In 2016 data according to Business Insider data shows that the Fintech “funding volumes” decreases year over year looking at 2016 vs 2015. The number was about 12.7 million in 2016, so about 13% down from the 14 billion dollar number in 2015. However, the number of deals stayed around the same, indicating that it was the size of the deals that caused this decrease in funding volume. There are a few potential factors that could account for this. Due to the large amount of funding in 2015, that may have left less money from VC companies to fund fintech companies in 2016. We may even see that trend continue into 2017. In fact the article notes that if not for two large deals in China the year over year decrease in VC funding of Fintech companies would amount to around 28%. There was more caution in the overall market in 2016 as well, and that could have also led to a lower amount of funding overall by VC firms. However, looking at the potential for Fintech companies, especially in today’s business environment, there is ample room for market disruption which could pave the way for record funding numbers. This extends to emerging fintech sectors such as P2P lending, online banks, and fintech “robo” advisors. Looking at 2017 will give a better idea of the direction that the fintech funding numbers will be trending.

http://www.businessinsider.com/fintech-deal-sizes-are-shrinking-2017-2

Fintech solutions in Indian economy

Here are my views about Fintech in India:

Fintech companies in India are solving some basic but important problems in the emerging economy time and change amount. Nearly 66% are in payment processing and banking. Three major reasons for success are the convenience, transaction charges and trust. Companies like Paytm -an e-wallet company are able proving bill payment such as electricity, telephone etc. and ticket booking services at the user’s convenience. This may not be new to developed countries but in India previously People need to go to the concerned office and wait in line for hours office to pay the bills. E-wallets also solved an important problem of change amount.An average Indian would do nearly 4 to 5 cash transactions, because of e-wallet, they need not worry about the exact change in their transactions. In addition to this, they are also disrupting banking sector, companies like BankBazaar, a startup that lets Indian consumers compare financial products online giving more freedom to the customers not to depend on a single bank or insurance for their needs. I feel that going at the current pace it would solve many other problems in the Indian economy like micro insurance etc.

https://en.wikipedia.org/wiki/FinTech_in_India

http://www.financialexpress.com/industry/towards-a-fintech-revolution/262870/

Climate of Fintech Startups

The article “Please Don’t Start a Fintech Startup” describes exactly what it sounds like – reasons why to not start a startup in financial technology. Author Matthew Hughes cites several reasons, including complicated and restrictive regulations and difficulty with successful user experience. The argument he writes is convincing, detailing quotes from many fintech startups CEO’s, with experiences such as difficulty with consumer verification and security concerns. These certainly present numerous challenges to any entrepreneur looking to enter the fintech field.

Hughes makes many valid points. Fintech startups do seem difficult, and would require time and energy. However, he even states that “there’s a certain allure to the fintech space. Financial services are old, stodgy, and in dire need of shaking up.” I believe that being afraid of regulations is not an excuse to abandon innovation. Hughes says himself that the industry desperately needs some disruptive innovation. While I understand the difficulties they present, his choice to not enter this market does not mean he should discourage others. Imagine if the creator of the credit card felt overburdened with regulations? Financial technology would be greatly different today. So, in conclusion, if you have an idea that could be successful, it should be pursued, and who knows what kind of change you could make in the fintech market.

Source: https://thenextweb.com/finance/2017/02/15/please-dont-launch-a-fintech-startup/#.tnw_JTbqt1of

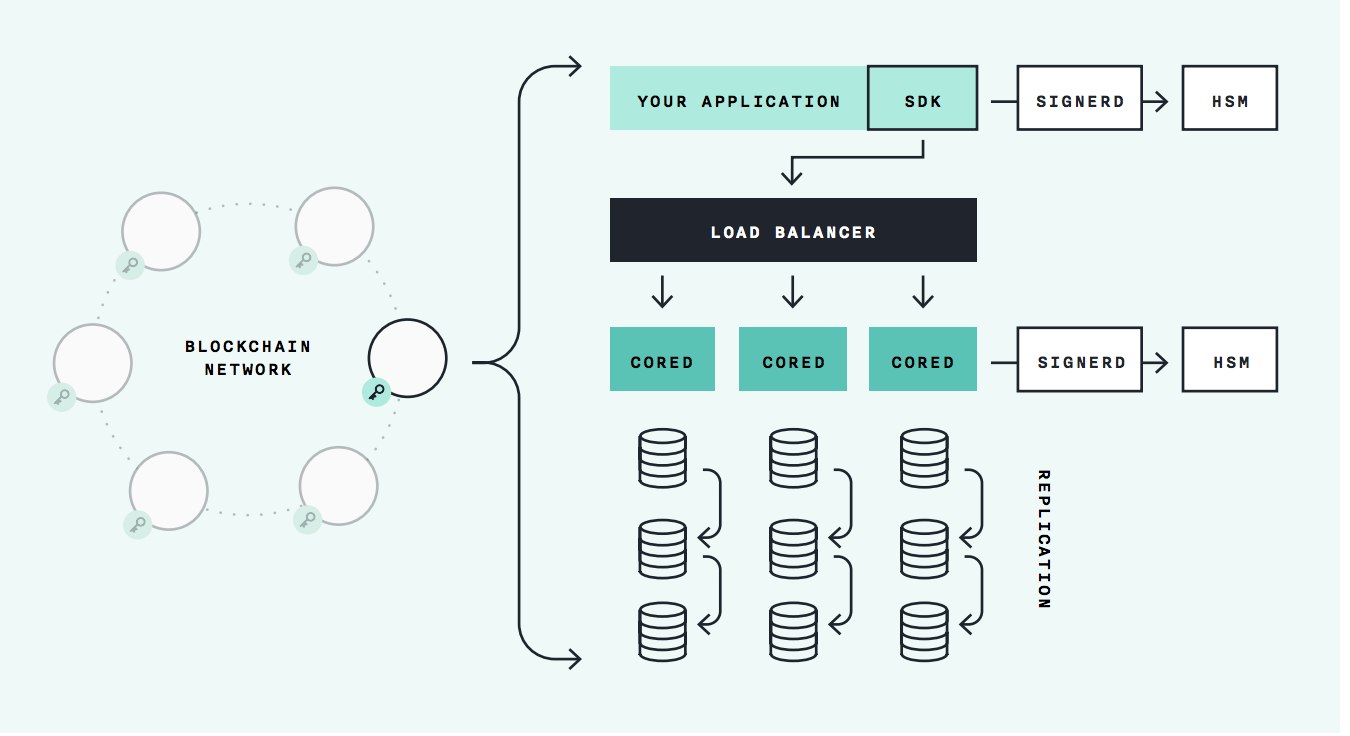

Blockchain Infrastructure: Chain Inc.

Chain Inc. Company Overview: Chain Inc. partners with leading financial institutions to build and deploy blockchain networks that enable seamless, programmatic and peer-to-peer transfer of digital assets. The platform, which is based on the open and interoperable bitcoin protocol, enables institutions to create, issue, store and transfer digital assets on private networks purpose-built for a given market. Founded in 2014, Chain Inc. is headquartered in San Francisco, CA. Chain Inc. Venture Funding: The company has raised $43 million in equity funding from a syndicate of financial and payments industry leaders including Visa, Nasdaq, Citi Ventures, CapitalOne, Fiserv and Orange.

Chain Inc. Product (Chain Core): Chain Core is an infrastructure software that enables institutions to issue and transfer financial assets on permissioned blockchain networks. Chain Core is engineered for the performance demanded by modern financial systems. The time to create, finalize, and settle a transaction is measured in milliseconds. Because its goal is to modernize the backbone of financial services, Chain Core supports today’s volume of transactions and beyond. Scalability is a key design principle of Chain Core. The image below is displays the architecture of Chain Core.

Chain Core Features:

- Chain Core enables organizations to launch and connect to blockchain networks that operate on the open source Chain Protocol.

- Chain Core-enabled blockchain networks facilitate transactions between entities directly. These transactions can serve to issue new assets, transfer assets between parties, or retire assets.

- Chain Core also allows entities to originate assets and issue them onto a network.

- Chain Core uses cryptographic public/private key pairs to keep track of identities, accounts, and ownership.

References:

- https://www.crunchbase.com/organization/chain-2#/entity

- https://chain.com/technology/

Traditional Banking Vs FinTechs

The financial services sector is bracing itself for an unprecedented period of disruption. Innovations such as smartphones, big data analytics, and the blockchain technology that underpins Bitcoin, are forcing banks, insurers, and Wall Street firms to adapt to an unpredictable future where some of the old rules no longer apply.

The FinTech revolution accelerated with the new regulations enacted in the wake of the 2008 financial crisis, which made certain lines of business less profitable for banks and created an opening for startups leveraging big data, new communications modalities, and other tools to serve more tech savvy consumers. At first, banks began trying to develop many of these technologies themselves in a bid to keep up with their rivals. But as the pace of innovation has accelerated, banks have found it harder and harder to do everything at the pace, volume, and scale required.

In order to assess which side will come out as a winner, it’s important to understand the core segments of the market.

SMB banking: After the 2008 financial crisis, heavy regulations were imposed on the banks, making it much more expensive to service SMB customers. This led traditional banks to pull back from this segment, creating a lack of available financial tools and resources for SMBs. Also, majority of surveys conducted recently state that small businesses face all kinds of barriers when applying for loans and other financial services in the U.S. FinTech startups have rushed into this void, offering more efficient technologies and tools for lending, payments, operations, underwriting, cybersecurity, know your customer, regulations, compliance, asset management, and more. This trend is expected to continue for new market leaders to be born in this category. The SMB market is the segment in which nimble FinTech companies are most likely to displace large banks.

Corporate banking: Banks will be wise to invest in this segment. Not only must they double down to remain competitive against rivals, but it is an area where startups will face the highest barriers. While some startups are likely to attack these segments, they are much less likely to be successful due to the complexity of the products and services, the need for large balance sheets, the regulatory scrutiny, and the ongoing strong relationships banks enjoy with their major customers.

to be contd…

https://www.romexsoft.com/blog/fintech-vs-banks/

https://letstalkpayments.com/fintech-and-traditional-banks-a-beginning-of-a-beautiful-friendship/

Out with the old in with new? Not just yet…

At a conference hosted by the Australian Prudential Regulation Authority, the chairman both praised and criticized the large increase in spending on new financial technologies in the banking sector. He is quoted saying “Companies must continue investment in existing technology platforms while at the same time putting money into new technology which may well replace it”. His main point was that we see a huge uptick in new services offered to consumers and how they do their banking, but if the back-end hardware gets outdated, it will no longer be able to support the increasing number of transactions it is being tasked with processing. That’s why it’s important to still continue to investment in the infrastructure of the financial system.

Chairman Byres makes a valid point because when you update everything about a system besides the processes that truly drive the system, it will eventually be less functional. It’s like paying $5,000 for upgrades like a stereo, rims, spoiler, etc, to a car that costs $1,000. From the outside, it may look nice and flashy, but it won’t be able to perform as good as it looks.

http://www.fintechbusiness.com/industry/642-don-t-get-distracted-by-fintech-toys-apra