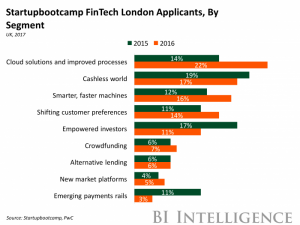

According to the article, fintech industry is reaching maturity as there are fewer new startups and it has observed a steady development from 2015 to 2016. It is not surprising that 3 segments that have had largest growth from 2015 to 2016 are cloud and core processing solutions; artificial intelligence, machine learning, blockchain technology; and customer segmentation and product personalization solutions. Their strong growth is thanks to the evolving technologies and customer willingness to adopt new offerings. Three segments that saw a declining trend are retail payment solutions; robot advisor so-called empowered investors; and emerging payments because firms in these areas have established strong positions and entry barriers.

It is predicted that we will see a lot of partnerships between startups which have been disrupting decades-old practices and traditional, larger players who have been rigorously developing their own innovations to adapt with those game-changing technologies. I believe that the convergences rather than fierce competitions will be beneficial for not only both parties but also consumers as they can offer more handy services at cheaper costs and become more profitable.

Source:

http://www.businessinsider.com/these-are-the-fintech-segments-most-likely-to-grow-in-2017-2017-3