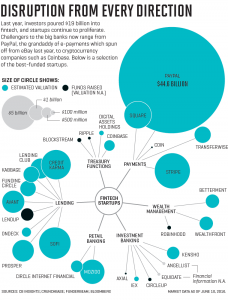

We have heard a lot of the positives of cryptocurrencies that operate on a blockchain network such as Bitcoin. Recently, the U.S. Securities and Exchange Commission on Friday denied a request to list an exchange traded fund built to track bitcoin. If accepted, this would have been the first digital currency fund in the U.S. Investors have been trying for more than three years to convince the SEC to allow a Bitcoin ETF to be on the market. Because of the rejection of the ETF, the digital currency’s price plunged as much as 18 percent following the decision. Investors speculated that if there was an ETF holding, the digital currency would get more individuals to buy the asset. Part of the reason why the ETF was denied was because the commission believed that bitcoin is unregulated and it is relatively in its early stages of development. In addition, there is question on if the regulators would be able to price and trade the fund effectively. This is interesting that even though bitcoin is on a blockchain network, ensuring that it is not able to be hacked, the SEC rejected the application. It is possible that soon in the future, Bitcoin will apply again and have its own ETF.

Article: http://www.cnbc.com/2017/03/10/us-sec-rejects-application-to-list-bitcoin-etf.html