Frauds alone in the banking sector cause losses in billions every year. In the United States alone, this number has hit $12billion in losses with a staggering 15% increase from the year 2015. These numbers are pretty huge and pose the single biggest challenge to banks and their customers world wide. Apart from the risk of losing customers, direct financial impact for banks is turning out to be a significant factor. Listed below are a few business drivers that help detect and prevent fraud in retail banking:

- Risk of losing customers: Fraud generally erodes the trust customers place on their banking partners leading to higher churn rate making customer acquisition difficult.

- Financial losses: Banks are generally charged with penalties in case a fraud occurs, not only are they liable for the transaction costs, merchant chargebacks but also have to pay regulatory charges.

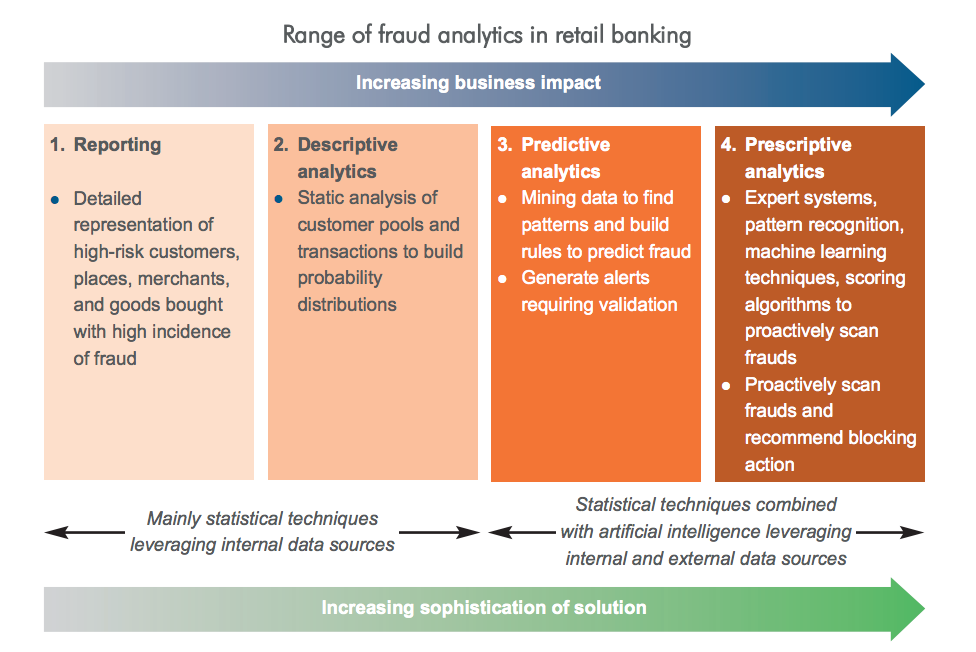

Fraud Analytics: Fraud analytics combines technology analysis and techniques along with human interaction to help detect potential fraudulent transactions in a business process, either before the transactions are completed or after they occur. The process of fraud analytics involves gathering and storing relevant data and mining it for patterns, discrepancies, and anomalies. The image below displays the range of fraud analytics deployed by banks to help detect fraud.

Benefits of Fraud Analytics in Banking:

- Analytics helps improve the ability of existing fraud experts to focus specifically on real threats by expanding the range of transactions that need to be monitored and reducing the number of fraud alerts. Fraud Analytics is done by pulling out data across various business processes onto a central system, helping create a enterprise wide view that makes it easier to trace back the origin of fraud

- Advanced analytics helps in recognizing patterns of fraudulent transactions, and play a key role in predicting the possibility of the next fraud that might occur with an intention to recommend preventive measures.

In conclusion, as transactions become virtual and their volumes grow rapidly, there is no stopping fraud. Rapidly growing technology is an enemy and opens up several avenues for fraudsters. Banks need to adopt emerging best practices to successfully operationalize fraud analytics. Designing self-learning algorithms that learn from the positive identifications they make and continuously updating and refining the models can help banks be one step ahead of fraudsters.

Reference:http://www.genpact.com/docs/resource-/fraud-analytics-in-retail-banking—detect–deter–and-prevent