This week in class we familiarized ourselves with the procurement process and the role of Financial Information Systems in automating the procure-to-pay process. Global universal banks have traditionally dominated Supply Chain Finance’s competitive landscape, but over the past few years, a multitude of fintechs have entered the market providing platforms and software-based services to support the Supply Chain Finance operations. These fintechs have revamped their value proposition by offering innovative business models, improved digital interfaces and rapid innovation in response to buyer and supplier feedback. So what exactly do fintechs bring to the table as opposed to traditional banks?

- Focus on improving the operational capability through online tools to help suppliers onboard. Provide digital modules for training on how to use systems.

- Ability to analyze spend-working capital status.

- Ability to access the most credit capacity.

- Attractive price offerings to suppliers.

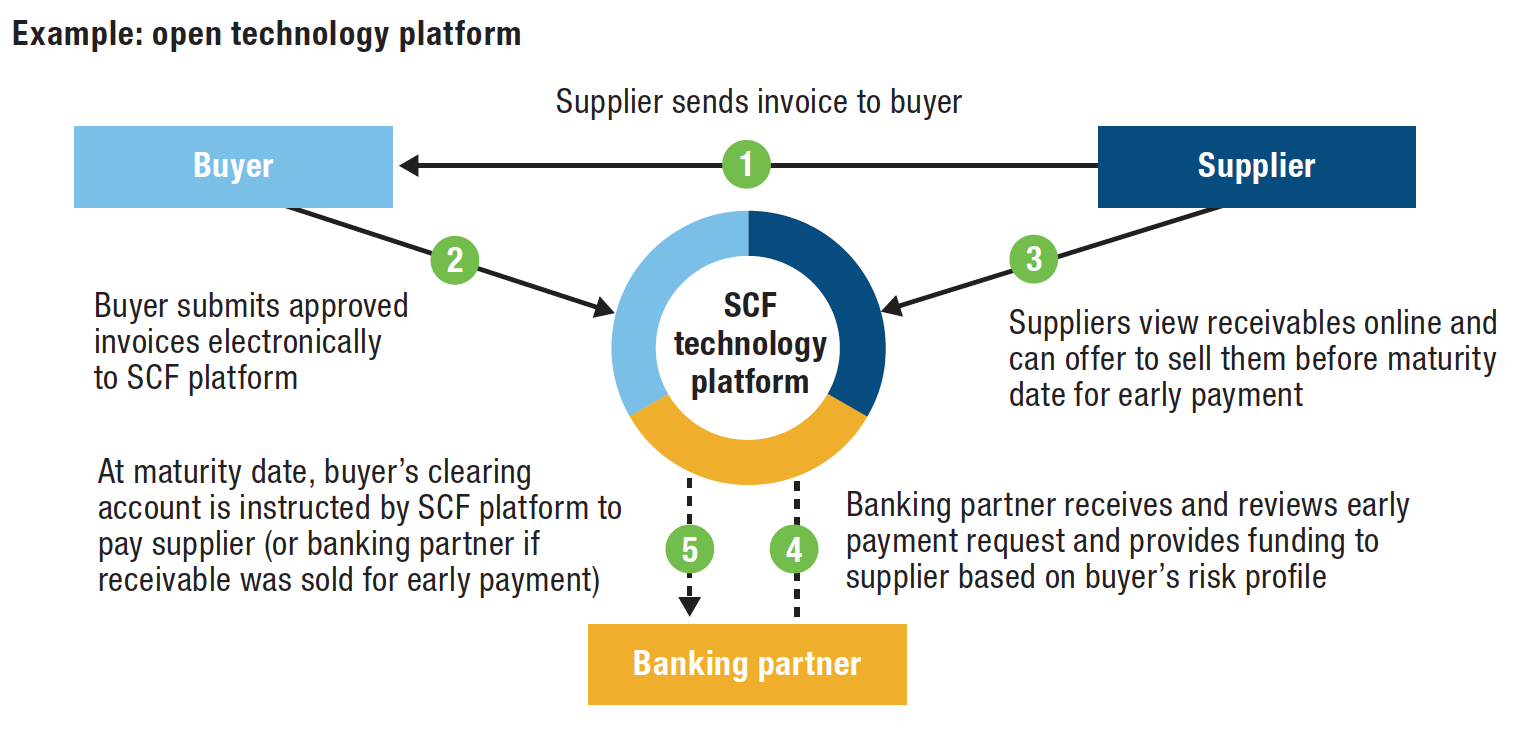

The image below, shows the emergence of technologies that connect counter parties that have enabled the growth of the Supply Chain Finance landscape.

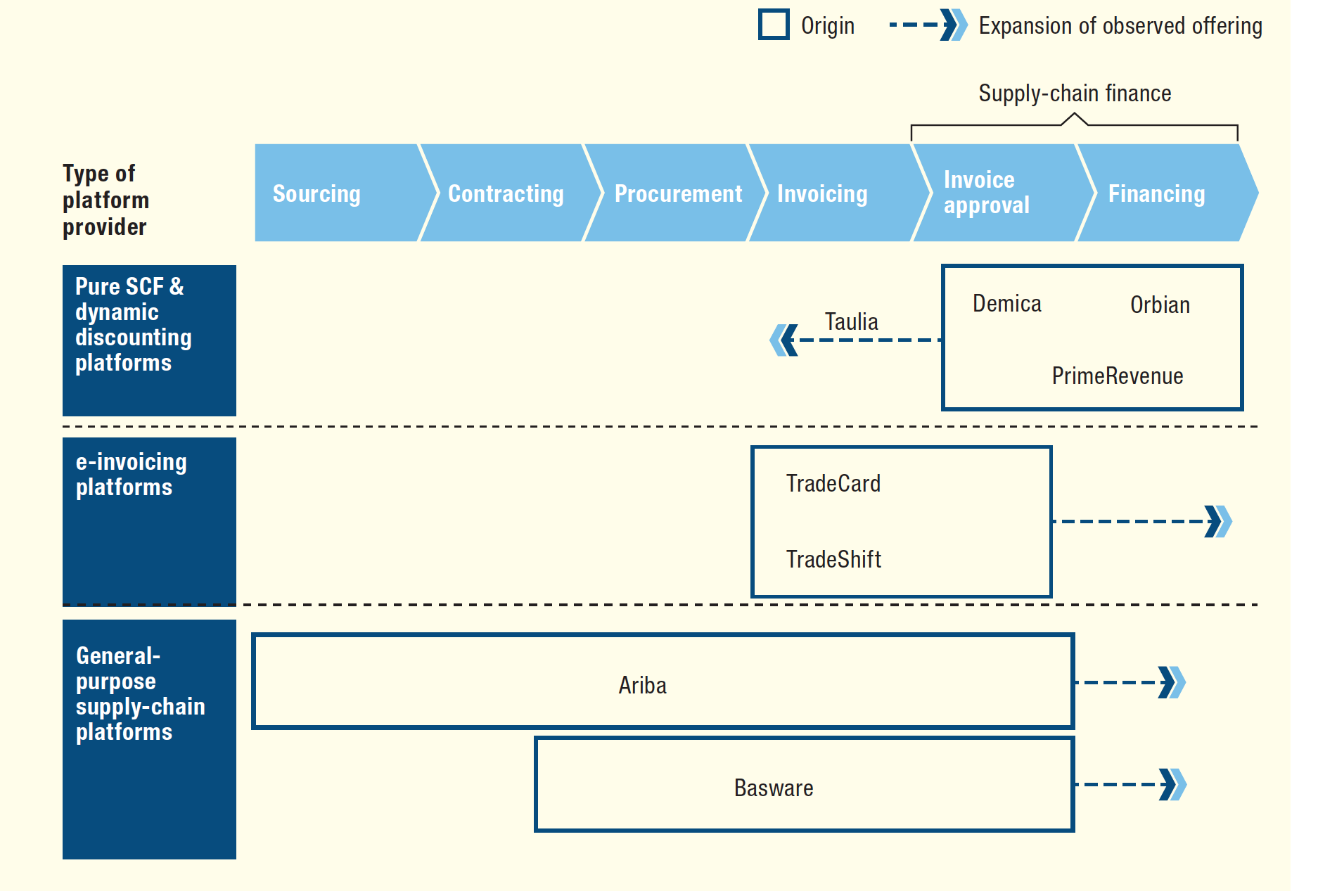

Fintechs are also looking beyond the pure Supply Chain Finance products and seeking to provide solutions for needs across the procure-to-pay cycle. The image below displays the various platforms provided by Fintechs in an ideal procurement process.

Having said that, it’s not all doom for the banks yet. They need to act fast to cope up with the challenges posed by Fintechs.

- Banks need to identify gaps in their technology offerings and either develop innovative solutions or partner with fintechs to do so.

- They also need to review their current portfolio and identify opportunities to improve performance by perfecting operational capabilities within their existing programs.

In conclusion, the Supply Chain Finance landscape is approaching towards an inflection point, and the winners will be the banks and fintechs that partner with each other to leverage funding and technological strength and continue to innovate with a deep understanding of the needs of both buyers and suppliers.

Reference: http://www.mckinsey.com/~/media/McKinsey/Industries/Financial%20Services/Our%20Insights/Supply%20chain%20finance%20The%20emergence%20of%20a%20new%20competitive%20landscape/MoP22_Supply_chain_finance_Emergence_of_a_new_competitive_landscape_2015.ashx