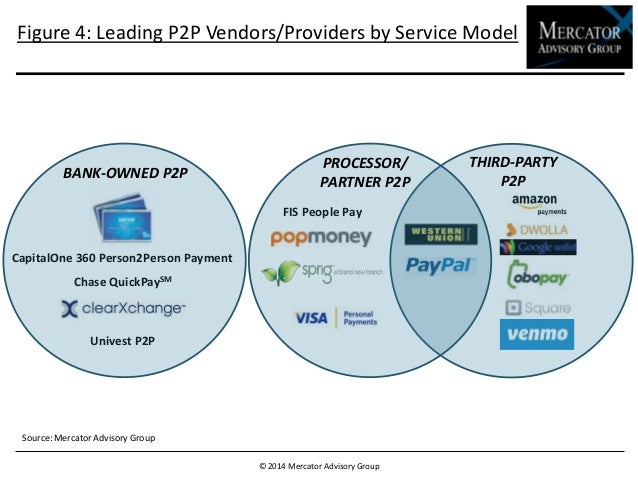

1) Bank-owned P2P model: In this model, the sender’s bank does the transfer of funds. There are a number of banks which operate in this way. The financial institutions have developed their own applications so provided P2P service.

Example :

clearXchange: It was founded in 2011, and it was owned by Bank of America, Capital One, JPMorgan Chase, US Bank, and Wells Fargo. Customers of either of the banks could send/receive payments. The sender only has to enter the recipient’s email or phone number. It was sold to Early Warning in 2016 and rebranded as Zelle.

2) Processor/partner P2P model: In this model, the sender’s bank uses a processor/partner to transfer the funds.

Example:

PopMoney was developed by Cashedge is now a part of Fiserv. Popmoney is slightly different from other P2P payment services in the sense that the transactions execute from sender to receiver directly, eliminating the need for a stored value account. Pop is an acronym for “pay other people” and provides services for several banks and credit unions.

3) Third-pparty-ownedP2P: In this model, the sender interacts with a third party to transfer the funds using ACH or credit/debit cards. This is the most popular model and there are a number of players in the market such as Google Wallet, Amazon, Dwolla, Venmo, and Square Cash. PayPal is the most widely used service. In 2015, PayPal processed $41 billion in mobile person-to-person payments, up 42% from 2014.

References:

http://www.paymentsjournal.com/WorkArea/DownloadAsset.aspx?id=22928